Conet TECH

Continental Network Technologies

Case Studies

Conet-Tech Case Studies

Mercer Canada

Case Overview

As employees take on increasing responsibility for their retirement planning, many are losing ground in the quest to become retirement ready. This has serious implications for individuals, companies and society alike. It’s time for a more balanced solution for retirement planning — one that offers employees control over their financial choices while providing enhanced employer guidance and oversight.

Traditional methods of evaluating retirement programs won’t tell you whether your program is meeting its core objective: to help employees achieve a comfortable retirement at a reasonable age. Mercer’s Retirement Readiness Analytics is an enhancement to traditional analysis. We evaluate your employees’ “retirement-ready age” to help you figure out which actions will have the biggest impact on their financial well-being.

Mercer’s plan is to help organizations evaluate employees’ “retirement-ready age” and determine which actions are likely to have the biggest impact on their financial well-being.

Customer Overview

At Mercer, they make a difference in the lives of more than 115 million people every day by advancing their health, wealth, and careers. They’re in the business of creating more secure and rewarding futures for their clients and their employees — whether they’re designing affordable health plans, assuring income for retirement, or aligning workers with workforce needs. Using analysis and insights as catalysts for change, they anticipate and understand the individual impact of business decisions, now and in the future. They see people’s current and future needs through a lens of innovation, and their holistic view, specialized expertise, and deep analytical rigor underpin each and every idea and solution they offer. For more than 80 years, they’ve turned their insights into actions, enabling people around the globe to live, work, and retire well. At Mercer, they say they Make Tomorrow, Today.At Mercer, the goal is to make retirement work for everyone — retirees, younger employees, and the organization. Currently, a combination of unintended consequences is casting a shadow over the entire retirement process.

Mercer provides clients with a holistic approach to pension risk management — one that aligns strategy with the plan’s overall funding status. Mercer’s pension risk consultants have expertise in developing sophisticated strategies that include:

- Setting glide paths and de-risking levels.

- Integrating risk management with funding improvement

- Liability-driven investments

- Derivatives

- Buyouts

- Risk-transfer scenarios

Business Challenge

Anyone is managing a defined benefits plan today faces persistent risks and evolving realities: market volatility, uncertain liabilities, shifting regulations, and pressure to reduce expenses and contributions. Succeeding in this landscape requires an agile strategy and process that can dynamically react to market conditions and seize opportunities while managing risk and expense.Conet-Tec security team performs realtime security assessments on web applications. These assessments aim to unconver any security issues in the scanned web application, explain the impact and risks associated with the found issues, and provide guidance in the prioritization and remediation steps,

The objective of this assignment was to perform controlled attack and penetration activities to assess the overall level of security of the retirement system.

The technologies

- Visual Studio .NET and Microsoft .NET Framework, VB.Net, ASP/ASP.Net MVC- Windows Server and SQL Server Enterprise Manager, IIS, VECMA, AODA

- AppScan, SOAP Web Services, WCF, SOA, UAS

- MS Excel for the calc engine

Solution

Mercer experts and Conet-Tech consultants built a new retirement system and go beyond participation levels, contribution amounts and investment returns and determine whether a retirement plan is actually meeting its core objective: To help employees achieve a comfortable retirement at a reasonable age. Our solution can also boost retirement plan strategy through enhanced communications, more effective plan designs, micro-targeted education campaigns and investment structure adjustments.Additional delivery: MRA Security Remediation – Application Security Management - Worked in joint application development environment with cost-effective L&T resources in India to remediate and reduce the security vulnerabilities based on AppScan tool report of 82 VECMA and MRA US and Canadian retirement applications. Common application security issues resolved include Cross Site Scripting, SQL Injection,

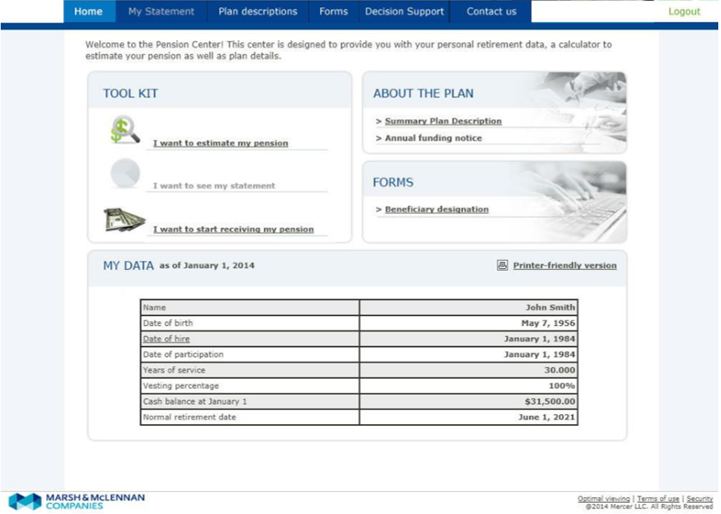

The main module is composed of two sections, Personal Data and Assumptions and Results.

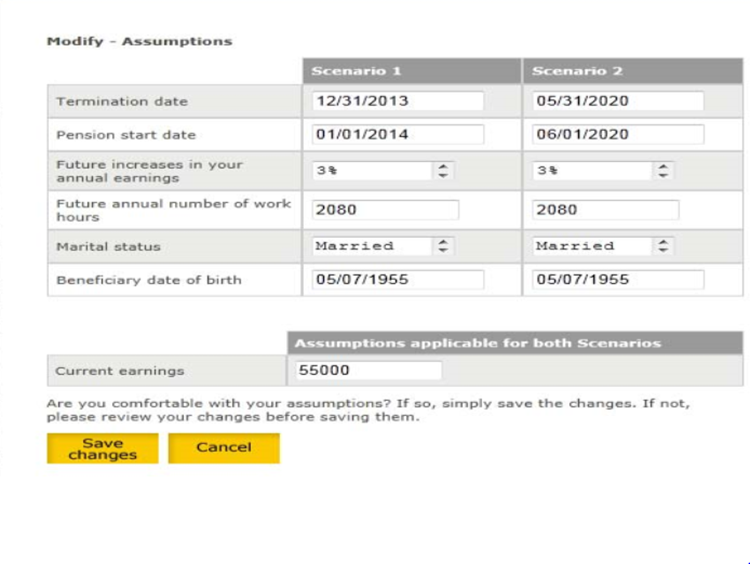

Personal Data and Assumptions

- My personal data: The user sees his/her personal data. He/she is requested to contact the client organization Pension Center if the data is not accurate.

- My assumptions: The user sees the default assumptions. He/she can modify the calculation assumptions

Validations Based upon the available assumptions that a user can modify, certain validations will be performed on the web. The data is validated for the two available scenarios simultaneously and any appropriate error message is displayed when the user clicks on Save changes.

Results

Payment options: The user sees the estimated pension under:1. Single Life Annuity Provides monthly benefit payments to you during your lifetime. No benefits will be paid after your death. If you are married, your spouse must provide written consent to your election of this form of payment. Note: Once benefit payments begin, you may not change the form of payment that you have elected.

2. Increasing Single Life Annuity Provides monthly benefit payments to you during your lifetime. The benefit amount will increase by 2% compounded annually, effective each annual anniversary date of your benefit commencement date. No benefits will be paid after your death. If you are married, your spouse must provide written consent to your election of this form of payment. Note: Once benefit payments begin, you may not change the form of payment that you have elected.

3. 50% Joint & Survivor Annuity Provides reduced monthly payments to you during your lifetime. In the event of your death, your designated beneficiary will receive monthly benefit payments equal to 50% of the amount you had been receiving for the remainder of his or her lifetime. If you are married, your spouse must provide written consent to your election of this form of payment and to any non-spouse beneficiary you name. Note: Once benefit payments begin, you may not change the form of payment that you have elected. Additionally, for this option, you may not change your beneficiary designation after benefit payments begin.

4. 50% Joint & Survivor Annuity Provides reduced monthly payments to you during your lifetime. In the event of your death, your designated beneficiary will receive monthly benefit payments equal to 50% of the amount you had been receiving for the remainder of his or her lifetime. If your beneficiary dies before you, your benefit will be recalculated and paid to you as a life-only annuity. If you are married, your spouse must provide written consent to any non-spouse beneficiary you name. Note: Once benefit payments begin, you may not change the form of payment that you have elected. Additionally, for this option, you may not change your beneficiary designation after benefit payments begin.

5. 100% Joint & Survivor Annuity Provides reduced monthly payments to you during your lifetime. In the event of your death, your designated beneficiary will receive monthly benefit payments equal to 100% of the amount you had been receiving for the remainder of his or her lifetime. If you are married, your spouse must provide written consent to your election of this form of payment and to any non spouse beneficiary you name. Note: Once benefit payments begin, you may not change the form of payment that you have elected. Additionally, for this option, you may not change your beneficiary designation after benefit payments begin.

6. Lump Sum Provides your entire benefit in a single payment to you. No benefits will be paid after your death. You may directly receive the lump sum payable to you or roll over the amount into another eligible employer plan, Individual Retirement Account (IRA) or Roth IRA. If you elect to receive your benefit as a single lump sum payment, the law requires that 20% of the taxable portion of your distribution will automatically be withheld and applied to your federal income tax for the year in which the distribution is made unless you elect to have your distribution paid as a direct rollover to another eligible employer plan or to an individual retirement arrangement (an IRA). Please read the Special Tax Notice Regarding Plan Payments. If you are married, your spouse must provide written consent to your election of this form of payment.

7. PBEP Lump Sum. The Pension Benefit Equalization Plan (PBEP) is designed to provide you the amount of the retirement benefit you would have received under the Dex One Retirement Account had the IRS Code compensation limits not applied, less the actual benefit you will receive under the